THANK YOU, CAPITALISM:

Why Are Berries Everywhere, in Every Season? Driscoll’s: .The California giant has helped turn a local, seasonal treat into a worldwide refrigerator staple and marketing juggernaut. (Julia Moskin, July 7, 2026, NY Times)

Once upon a time, there was only one way to get your hands on a ripe strawberry in winter: be a member of the French royal court.In 1712, Louis XIV dispatched a spy to Spanish-controlled Chile to smuggle out native white-berried plants. Royal gardeners bred them with European red berries, coddled them in manure hotbeds and warmed them with underground fires, all so that the king could have strawberries in March instead of waiting until June.

Today, Costco shoppers in South Korea, pastry chefs in Dubai and parents of small children nearly everywhere can buy strawberries, raspberries, blueberries and blackberries any time of year — if they can afford them. (Strawberry prices fluctuate throughout the year, from about $3 per pound in San Francisco to $35 in Dubai.) And the biotech that drives modern agriculture ensures that each berry is better than anything the Sun King ever tasted.

ImageAn 18th-century still life of raspberries in a bowl.

Native strains of European strawberries produce fruit only in the summer, but centuries of hybridization have changed that.Credit…Heritage Images/Getty Images

In just the last decade, berries have completed the journey from fragile, local, seasonal treat to worldwide refrigerator staple and marketing juggernaut. Global production has tripled since 2000, according to research from the U.N.’s Food and Agriculture Organization, and still cannot keep up with demand. In sales and volume, berries are the fastest-growing category in American produce, according to data from the U.S. Department of Agriculture.Most of that growth has been driven by Driscoll’s, a $7 billion California company that began as a multifamily farm in 1904, patented its first strain of strawberries in 1958 and is still controlled by family members.

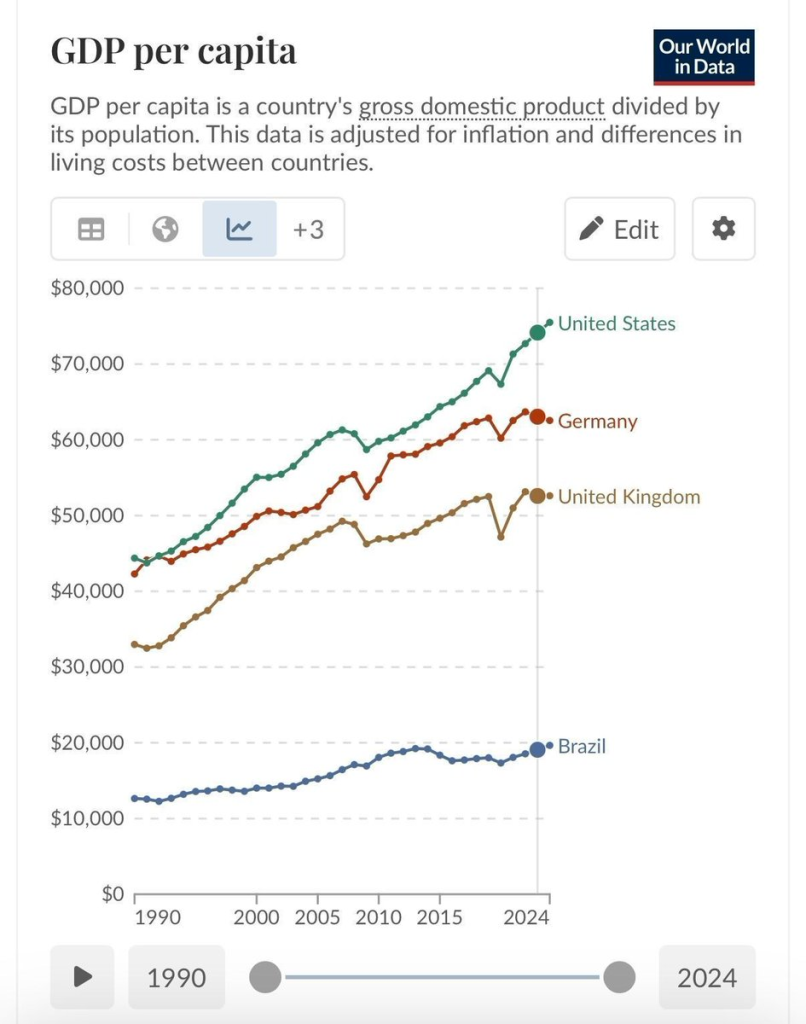

We are so affluent, we take living better than royalty for granted.